Why Richard, former hedge fund manager, chose Frec for direct indexing

Richard is a self-described bit of a nerd. When it comes to investing, he likes to look under the hood to examine the intricacies of the many offerings before deciding to invest — or more commonly, deciding not to invest.

He got his start in international commercial banking, then shifted to global capital markets, and finally into hedge funds where he co-founded several emerging markets-focused funds in the 1990s, with stops at JPMorgan and Merrill Lynch along the way.

More recently he’s turned to teaching others about finance. For the past three years, he’s been teaching finance at the Poznań University of Economics and Business on topics like alternative investments and wealth management. As part of this second career, Richard has earned a PhD in finance.

Before Frec

Richard likes to look deeply into things before he invests in them. In his opinion, “There are a lot of things on Wall Street where if you really start to look at how they work, you find out that they don’t really work.”

Direct indexing is not one of those things. It’s the rare investment product that meets Richard’s quality bar.

When Richard learned about direct indexing and tax loss harvesting a few years ago, he was quick to understand their value. His take?

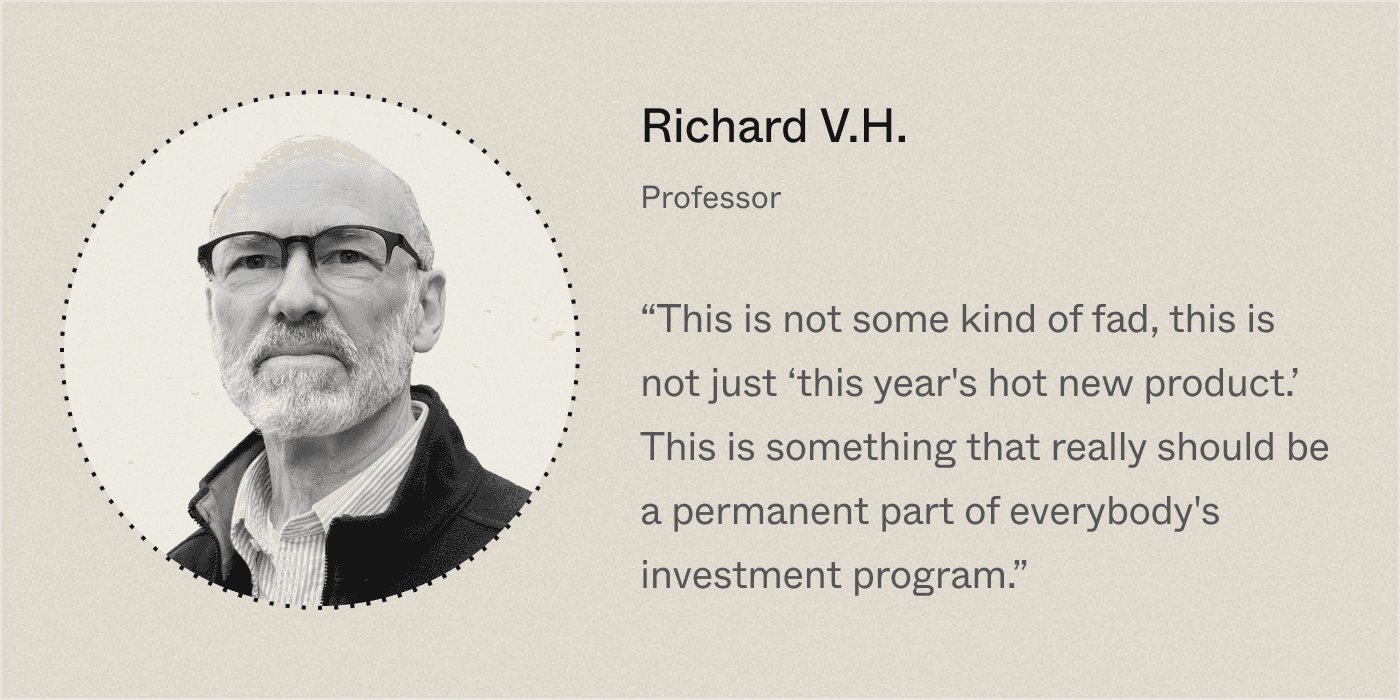

“This is not some kind of fad, this is not just ‘this year’s hot new product.’ This is something that really should be a permanent part of everybody’s investment program.”

“In the past, ETFs surpassed mutual funds in popularity due to ETFs being a superior investment product. Looking forward, direct indexing may well one day replace ETFs. People are going to recognize that having a passive indexing account at places like Frec is better than owning an ETF.”

Searching for the right product

Richard already knew he wanted to utilize direct indexing and tax loss harvesting in his own portfolio. But none of the products he saw on the market were quite what he was looking for.

One shop wanted him to pay 1% per annum on his assets, plus an additional 0.20% to use their direct indexing platform. That pricing didn’t work for Richard. Another shop he called charged 0.25%, “but I didn’t like the way the product was structured. They forced clients to put money into their asset allocation program in order to get access to direct indexing sleeve.” Yet another shop told him their tax loss harvesting product was available to clients of financial advisors but not to the company’s own direct long-time customers. In other cases, the minimum investment sizes were prohibitive.

Ultimately, Richard signed up for a tax loss harvesting account that charged 0.40%. He was happy with the performance, especially since the market was in a downturn in 2022 and there were plenty of losses to be harvested, “but I had this idea in mind that it really shouldn’t cost 0.40%.”

He kept looking for a product with lower pricing.

Why Frec?

Richard first heard about Frec on investor Howard Lindzon’s podcast. He went to Frec’s website and reached out to the team. He recalls being immediately impressed with both the product and the people.

The product

Richard found that Frec direct indexing “is superior to other products that are available in this particular field, because of the frequency of the harvesting — it’s daily.”

In addition, Frec’s tax loss harvesting is efficient “because they’re not treating each ticker as a holding, but rather each separate tax lot.” That means that instead of 500 holdings (one for each stock in the S&P 500), “I essentially have more holdings in my portfolio that can be analyzed on a daily basis for tax loss harvesting opportunities.” In other words, Frec’s awareness of the context of each lot of stock and the price it was purchased at, allows for more efficient loss harvesting than otherwise possible.

The price was also a major draw. At his previous brokerage, Richard was paying 0.40% for monthly harvesting, which delivered inferior results. “Here at Frec, they’re doing it daily, and… it’s priced at 0.10%, which is what it should be priced at.”

On the whole, Richard thinks Frec direct indexing has “a clear competitive advantage.”

The people

Richard is impressed with Frec’s product, “but the thing that really makes me feel good about sending hundreds of thousands of dollars into my account at Frec is the people. They’re experienced. They’re serious. And they’re available to clients who want to understand what it is that they’re actually investing in.”

Transparency

Richard always wants to know how his financial products work. At his previous brokerage, he found “there was zero ability to ask any questions or to find out anything about what’s going on inside the product.”

At Frec, by contrast, “I am welcome to ask questions. I can look under the hood.”

When Richard joined Frec, he spoke directly with a founding engineer and the Head of Brokerage Operations, and that played a big role in establishing trust. “There was no fluff, there was no marketing BS or anything like that. It was just the facts.”

While Richard knows that not everyone will care to do a deep dive, he thinks transparency in financial products is important. “Clients should have access to really understanding what they own.”

Recap

- Richard knows finance as well as anyone. He’s been a commercial banker, a VP at JP Morgan, and started several hedge funds. He also holds a PhD in Finance, and has spent the past three years teaching courses in asset management as an Associate Professor.

- He likes to look deeply into things before he invests in them. While he often finds that investments aren’t worth his time, direct indexing was the opposite—Richard thinks it “should be a permanent part of everybody’s investment program.”

- After learning about tax loss harvesting, Richard went on a quest to find the best direct indexing service on the market. Most places charged fees that Richard thought were unreasonably high, had inefficient harvesting strategies, and/or required high minimum investments.

- Frec was the winner. Frec’s daily tax loss harvesting, low fees, and $20,000 investment minimum made the product stand out. But what really sealed the deal for Richard was Frec’s high-quality team—and their willingness to let him look under the hood of the product.

“So, how do you get from hearing about it on a podcast with Howard Lindzon to sending hundreds of thousands of dollars worth of securities into this company that you hadn’t heard of before?” Richard asked rhetorically. “How do you get there?”

“It’s really two things together. First, it’s the product. But what made the path much easier was talking to the team. They are high-quality people, and that gave me the confidence to pull the trigger and put a bunch of money in Frec.”

This testimonial may not be representative of the experience of other customers. There is no guarantee of future performance or success.

Investing involves risk, including the risk of loss. Frec’s direct index product advisory services are provided by Frec Advisers LLC, a registered investment adviser. Brokerage services are provided by Frec Securities LLC, member FINRA/SIPC.

Frec Advisers LLC and Frec Securities LLC are both wholly owned subsidiaries of Frec Markets, Inc.